Business Credit Card Optimization: The Complete Guide for Owners

The money is already moving. The only question is who it pays.

Every business runs money through a card.

Materials. Fuel. Equipment. Software. Insurance. Subcontractors.

For an owner doing real volume, that is somewhere between $180k and $500k a year flowing through plastic.

Here is the part most owners never stop to check.

That money is already earning rewards. The only question is how much, and who it earns for.

Most of the time, the answer is "not much" and "the bank."

This guide walks through how business card optimization actually works, where the gaps usually hide, and how to fix them without spending an extra dollar.

What "optimization" actually means

It is simpler than it sounds.

Optimization means matching your spend to the cards that pay the most for it.

That is the whole game. You are not spending more. You are making the spend you already have work harder.

Three things drive it:

- Earn rate. What percentage you get back on a purchase.

- Category match. Whether your biggest spend lands on a card that rewards that category.

- Card mix. Using the right card for the right purchase instead of one card for everything.

Get those three right and the same spend can pay back two to four times more.

The three setups most owners are stuck in

None of these are mistakes. They are defaults. Nobody set the system up on purpose, so it runs at the lowest setting.

One. Everything on a personal or debit card.

Rewards earned: close to nothing. Debit earns zero. A personal card was never built for business categories.

Two. A plain 1% business card nobody chose.

It came bundled with the checking account. It works, but it pays the bare minimum.

Three. Spend scattered across four cards.

Nobody knows which card does what, so the rewards are split, forgotten, and never added up.

If you recognize your business in one of these, you are leaving money on the table every month.

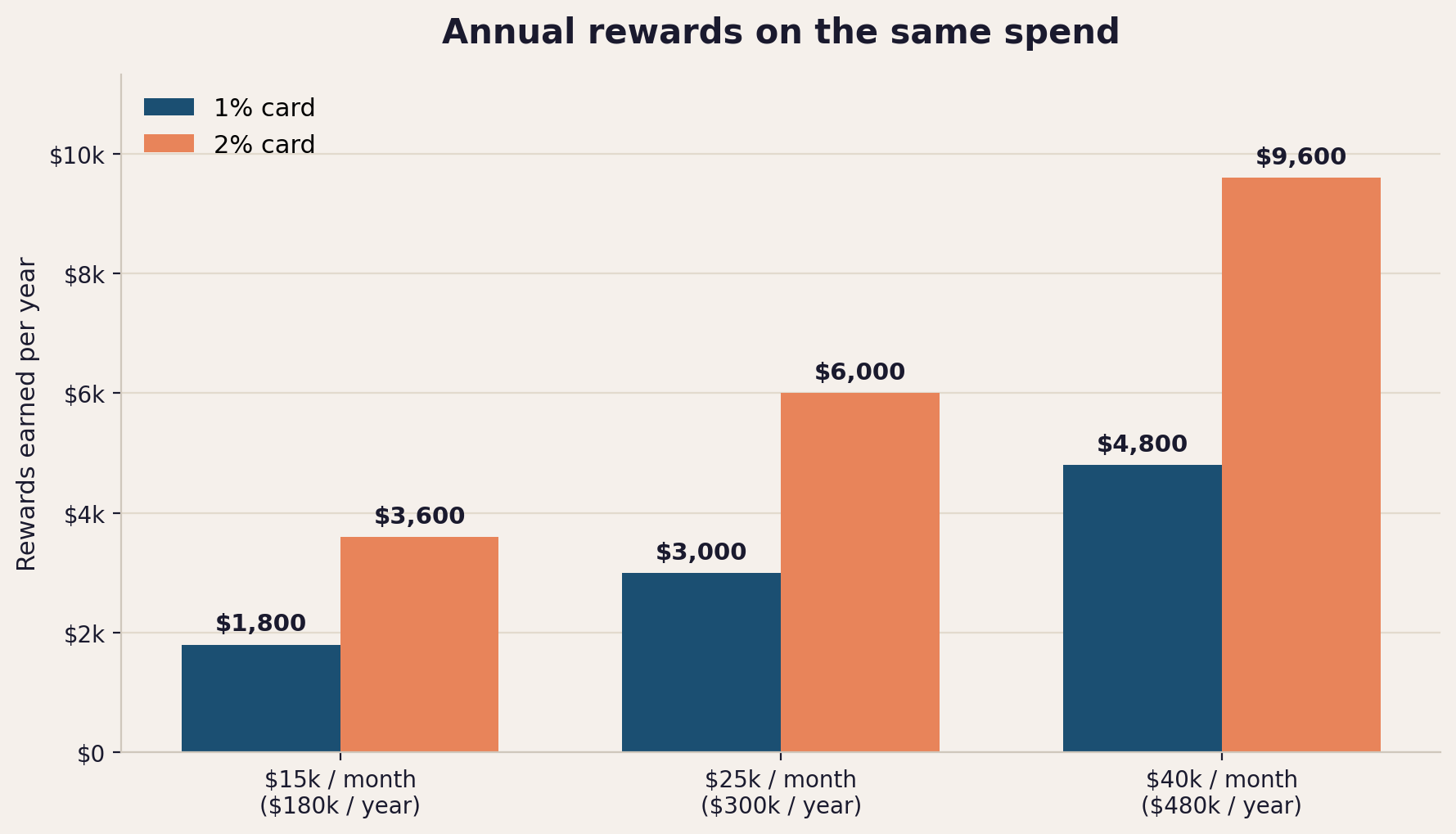

What the gap looks like in real numbers

Say you run $25k a month. That is $300k a year.

- On a 1% card, that earns $3,000.

- On a 2% card, the same spend earns $6,000.

Same purchases. Same business. Double the return.

Here is how that gap grows across spend levels.

That is the floor, not the ceiling. The chart only compares two flat rates. Cards built around specific spend categories can earn more on the right purchases.

The categories that matter most for trades

Most of a contractor's spend lands in a handful of buckets:

- Fuel for trucks and equipment

- Building materials and supplies

- Equipment and tools

- Insurance and recurring software

- Subcontractor and labor payments

The right card setup rewards your two or three biggest buckets at a higher rate, then catches everything else on a solid flat-rate card.

That split is where most of the upside lives.

Common mistakes that quietly cost you

Hitting earn caps without knowing it.

Some of the strongest category cards only pay the high rate up to a yearly spend cap. After that, the rate drops hard. An owner doing heavy monthly spend can blow through a cap by mid-year and earn next to nothing on the rest, with no warning.

Matching the wrong category.

A card that rewards travel does nothing for a business whose spend is fuel and materials. The card has to match where the money actually goes.

Paying an annual fee that does not pay for itself.

A fee is only bad if the rewards do not clear it. Plenty of fee cards return many times the fee. The mistake is paying the fee without running the math.

Treating the card as an afterthought.

The card sits in a drawer earning the lowest possible rate because nobody set it up on purpose. Twenty minutes of setup. Thousands a year. Every year after.

How to start fixing it

You do not need a finance degree. You need an hour and your last three statements.

- Pull your last three months of card statements.

- Add up your spend by category. Fuel, materials, equipment, software, everything else.

- Find your top two or three buckets. That is where optimization pays off most.

- Check the earn rate on your current card. If it says 1%, or you cannot find it, money is leaking.

- Check for any earn caps on cards you already hold.

- Match a higher-earning card to your biggest categories, and keep a flat-rate card for the rest.

That sequence is the core of every audit. Run it once and you will see the gap in your own numbers.

Get the free guide

We built a short guide that walks through the most common business card mistakes and what to do about each one. No card pitches. Just the math and the fixes.

You are already spending the money. Let's make sure it's paying you back.